It’s hard to remember now, but back in the early 2010s when we were all talking about social, local, and mobile, accelerators were pretty popular, too. By then, YC was clearly working (Reddit, Airbnb, Dropbox), and a number of people tried to copy, compete, or complement it.

SiliconAlley (I believe) ran an April Fools’ story sometime around then announcing “25 Accelerators,” an accelerator for accelerators backed by Ron Conway and Yuri Milner — it was funny because it was plausible. Universities and regional councils were spinning them up left and right.

These days, people in the startup world don’t really talk about “incubators.” Instead, they mostly talk about YC.

One frequently-told joke is that there are no moats in venture:

VC: Great startups build defensible moats against the competition.

Founder: So what makes you better than other VC firms?

VC: Mostly brand.

Fascinating, then, that YC has achieved that rare feat among investment firms — they’ve built a company with network effects!

Birth, growth, and differentiation

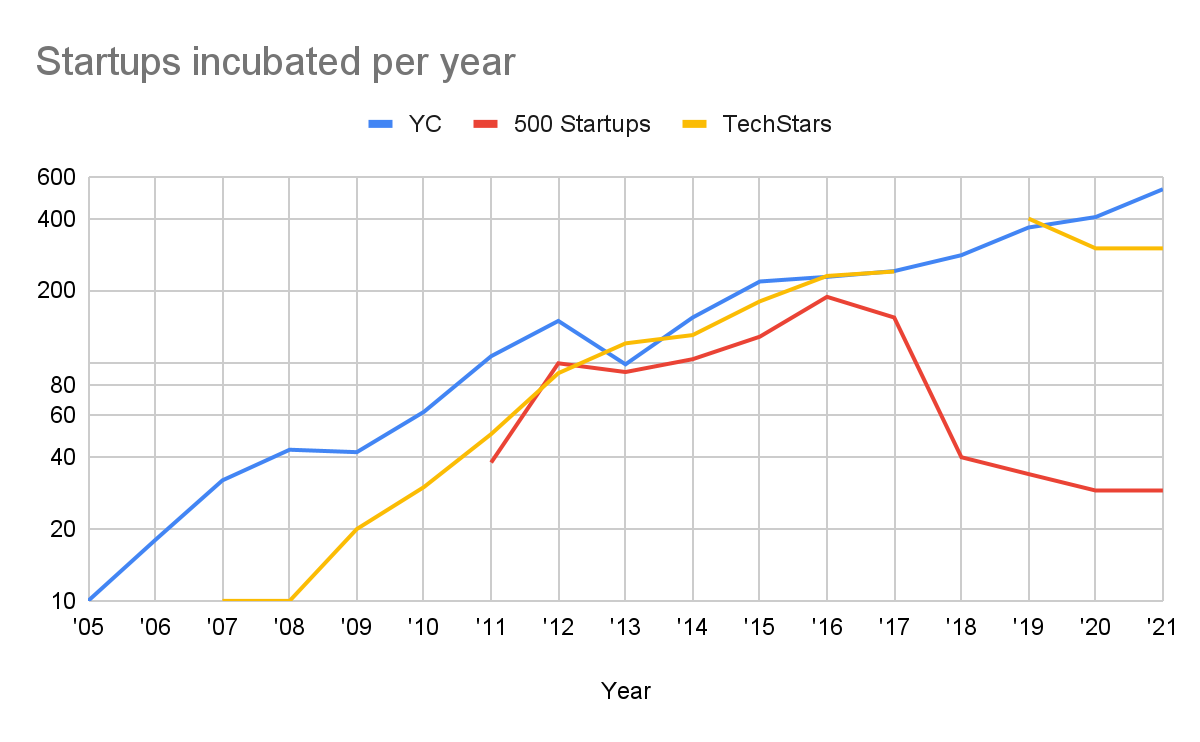

The three most prominent incubators started along similar timeframes:

- YC was founded by Paul Graham (pg) and Jessica Livingston in Boston in 2005 as a summer founders program; after splitting time between Boston and Silicon Valley, they moved entirely to SV in 2009.

- Techstars was founded in 2006 by serial entrepreneurs Brad Feld and David Cohen in Boulder.

- 500 Startups was founded In 2010 by Dave McClure and Christine Tsai in Silicon Valley,

Sources: YC Startup Directory, Mattermark, TechCrunch on 500; TechStars announcements

And while YC got started first, TechStars and 500 were able to grow to a similar scale fairly quickly, 500 by increasing batch size and Techstars by adding new chapters nationally and then internationally. The accelerators each adopted distinctive position on two axes: their target persona and location.

👤 Hackers, hustlers, investors

One way to think about incubators is that they’re a multi-sided marketplace, matching seed investors with technical cofounders and business co-founders to form startups and split equity.

YC appealed to technical founders. pg created new dialects of Lisp, wrote about why nerds hated high school, and called his forum “Hacker News”.

Whether or not this was a deliberate attempt to counterposition, 500 and Techstars were focused on the other personas.

500 targeted the business co-founder. 500 founder McClure: “YC is for Hackers and 500 is for Hustlers. They are chess nerds and we are band geeks. YC made Fire. 500 stole it…”

Techstars targeted seed investors and the early-stage ecosystem. Techstars founder Brad Feld wrote Venture Deals in 2011 as a detailed discussion of seed funding best practices, and Startup Communities as a case study of how Boulder, CO turned into a tech hub.

🏠 Silicon Valley vs. the world

While 500 joined YC in Silicon Valley, TechStars took a different approach, attempting to disperse knowledge and networks to new cities. This effort was roughly co-existent with Feld’s Startup Communities 2012 book launch, which made a huge splash in economic development, policy and media circles.

Public intellectuals like Richard Florida and nonprofits like the Kaufmann Foundation jumped on the bandwagon, as did some local civic/business promoter types like Dan Gilbert (Quicken) in Detroit and Tony Hsieh (Zappos) in Las Vegas.

Following that, TechStars opened up new incubator chapters across the country and then the globe, often working with local organizations to provide facilities and publicity.

In contrast, YC’s approach was to concentrate talent by bringing promising startups to Mountain View. Their marketing tended to run through Hacker News and focused on owning the developer water cooler.

Rather than constructing a supply chain of soil and fertilizer, their approach was to bring seeds to the greenhouse.

TechStars expansion by locale

| Timeframe | Description | New Incubators |

|---|---|---|

| 2010-13 | US secondary tech hubs | Seattle, Austin, New York, Boston |

| 2013-14 | Tech-adjacent US companies | Nike for sports, Sprint for mobile health, Disney for media, etc |

| 2016-17 | First-tier global cities, large US cities |

London, Berlin, Tel Aviv, Cape Town, Chicago, Atlanta, Paris, Singapore |

| 2017-19 | Second- and third-tier North American cities |

Montreal, Toronto, Minneapolis/St. Paul, Indianapolis, Kansas City |

| 2020-21 | Fourth-tier US cities, second-tier global cities | Des Moines, Birmingham, Portland ME, Munich, Abu Dhabi, Lisbon, Turin |

Cash in, cash out

The next natural question is, of course, how well did each approach work? Incubators are investment firms, and while return data isn’t public, investments are on standardized terms so we can make fairly reasonable estimates.

A good first pass is looking at the proportion of incubated startups hitting unicorn and decacorn status:

Proportion of unicorns by incubator

| Accelerator | >4yo firms | 🦄s | 🦄 rate | Deca-🦄s | Deca-🦄 rate |

|---|---|---|---|---|---|

| Y Combinator | 1.4k | 50 | 3.5% | 6 | 0.4% |

| TechStars | 1.1k | 9 | 0.8% | 0 | 0% |

| 500 Startups | 800 | 2 | 0.2% | 1? | 0.1% |

Sources: YC startup directory, TechStars portfolio; 500 portfolio; Mattermark

And we can get a bit more speculative, too! With fairly standard ownership terms, we can estimate returns. Let’s throw in a couple assumptions — uniform 3x dilution, equity held to exit — and round non-unicorns to zero:

Estimated returns by incubator

| Accelerator | >4yo firms | Inv. | Own. | Σ firm val. | Σ Inv $ | Σ stake val. | Return |

|---|---|---|---|---|---|---|---|

| Y Combinator | 1.4k | $100k | 7% | $480B | $140M | $11.2B | 80x |

| TechStars | 1.1k | $80k | 8% | $28B | $88M | $750M | 8.5x |

| 500 Startups | 800 | $125 | 5% | $13B | $100M | $220M | 2x |

YC’s estimated ~80x return is stunning. And they aren’t just paper markups — $360B of the $480B in company value they’ve incubated are from liquid decacorns that are either public or virtually so (Airbnb, Coinbase, Doordash, Dropbox, Stripe, Instacart).

Techstars’ ~8.5x return is strong. The bulk of their returns are coming from four unicorns (DataRobot, DigitalOcean, Outreach, and Remitly) valued between $4B and $6B that had recent uprounds and IPOs in the last 12 months.

500 Startups’ ~2x returns are okay. In fact, almost all of the results come from one soon-to-be decacorn, Talkdesk. Perhaps ths was one cause of 500 Startups’ circa-2017 incubation pullback; a 0.2% unicorn rate is not high enough to generate meaningful returns.

Why was YC’s approach the most successful?

To recap, YC’s approach was to find great technical founders and bring them to Silicon Valley. Why did this work so well in the 2010s?

Let’s start by looking for the macro trends. Since YC’s decacorns are driving three-quarters of its returns, we can reframe this in terms of “what made these companies so successful?“:

First, peer-to-peer vertical marketplaces have strong moats.

Six iconic peer-to-peer vertical marketplaces emerged in the 2010s, each worth between $20B and $100B: Airbnb, Doordash, Instacart, Coinbase, Uber, Lyft. YC incubated the first four, making over half of its returns.

Why were YC companies so successful in this space? Perhaps because peer-to-peer vertical marketplaces have strong moats. The key to winning is to move first and execute strongly to maintain your lead, until network effects shut out potential competitors.

These companies were all created in Silicon Valley by technical founders. They launched early, securing first-mover advantage; their companies excelled at using product design to reduce user friction, were mobile-focused, had highly quantitative product decision-making, and were impatient with a bias for action.

Second, there have been an explosion of bottoms-up B2B companies.

Over the 2010s, software became far easier to build, adopt, and charge for, leading to a huge proliferation of “product-led” B2B software companies. YC capitalized as young technical founders displaced enterprise software veterans.

YC decacorns & overall returns by sector

| Sector | Decacorns | Σ YC mkt cap | % of YC mkt cap | % of >4yo YC cos |

|---|---|---|---|---|

| Consumer: social & gaming | N/A | $0B | 0% | 9% |

| Consumer: other | Airbnb, Doordash, Instacart, Coinbase | $272B | 56% | 23% |

| B2B incl. fintech | Stripe, Dropbox | $189B | 39% | 44% |

| Traditional industries | N/A | $29B | 6% | 24% |

Third, Silicon Valley let companies raise $$$$ quickly and hire talent at scale

Each of the decacorns had a moment where they hit product-market fit, “went vertical” and 100x-d their valuation in three to four years, a pattern the Silicon Valley ecosystem is set up to support. And once they raised that money, they were generally able to hire the hundreds, and then thousands, of folks familiar with how to solve complicated product, technical, marketing, operational, and regulatory challenges. In the mid-2010s, these folks lived in Silicon Valley and were recruitable, first from Google and Facebook and then from each other, without relocation.

Decacorns pre-and-post growth valuation

| Firm | Date | Round | Amount | Valuation | Years | Multiple |

|---|---|---|---|---|---|---|

| Dropbox | Nov '08 | Series A | $6M | $25M | 3 | 160x |

| Feb '12 | Series B | $260M | $4B | |||

| Airbnb | Nov '10 | Series A | $7M | $50M | 3 | 100x |

| Oct '13 | Series C | $200M | $3B | |||

| Stripe | Mar '11 | Seed | $2M | $20M | 3 | 100x |

| Jan '14 | Series C | $80M | $2B | |||

| Instacart | Oct '12 | Seed | $2M | $20M | 2.5 | 100x |

| Jan '15 | Series C | $200M | $2B | |||

| Coinbase | May '13 | Series A | $5M | $20M | 4 | 80x |

| Aug '17 | Series D | $100M | $1.6B | |||

| Doordash | Sep '13 | Seed | $2M | $20M | 5 | 200x |

| Aug '18 | Series D | $250M | $4B |

Everything feeds talent density

So perhaps location and sector are useful macro causes of YC’s success. But startups are composed of people as well as business models — are there micro causes?

Let’s cast our net for accelerators a bit wider. Perhaps the real second place to YC isn’t TechStars, it’s 20 Under 20. Since it started in 2011, out of around 200 participants 20 Under 20 has generated five unicorns (Oyo, Scale, Upstart, Figma, Luminar), plus Ethereum, for a similar unicorn hit-rate to YC, albeit at a smaller scale.

So what differentiated 20 Under 20 and YC? Before he started YC, and in its first years, pg wrote repeatedly on the importance of clustering talented “makers” in a tight, small community. With his background in painting, he analogized Florence in the 1400s:

Most people who did great things were clumped together in a few places where that sort of thing was done at the time. (Cities and Ambition, 2008)

The inhabitants of fifteenth century Florence included Brunelleschi, Ghiberti, Donatello, Masaccio, Filippo Lippi, Fra Angelico, Verrocchio, Botticelli, Leonardo, and Michelangelo. Milan at the time was as big as Florence. How many fifteenth century Milanese artists can you name? (Taste for Makers, 2002)

The first five batches of YC, from S05 to S07 contained 60 companies with about 150 people. This included Aaron Swartz (Infogami S05), Steve Huffman & Alexis Ohanian (Reddit S05), Patrick & John Collison (Auctomatic W07), Emmett Shear & Justin Kan (Kiko S05), Sam Altman (Loopt S05), David Rusenko (Weebly W06), Jared Friedman (Scribd W06), Drew Houston and Arash Ferdowsi (Dropbox S07).

Of these, Dropbox was the only big financial return. But the Collison brothers came back for Stripe W09; Shear and Kan came back for Twitch W07 with Michael Siebel; Altman and then Siebel would go on to run YC after pg and Jessica Livingston stepped down. Shear still runs Twitch today.

And while Renaissance Italy is an evocative place to draw talent cluster analogies, there are others closer to home. In the last century and a half, America has spawned a number of local, sectoral golden eras:

- Industrials in Cleveland in from the 1860s to the 1890s (Standard Oil, Dow Chemical)

- Electricity in New York in the 1880s and 1890s (General Electric, Westinghouse)

- Autos in Detroit from the 1900s to the 1920s (Ford, General Motors, Chrysler)

- Film in Los Angeles from the 1910s and 1920s (Universal, Paramount, MGM, Disney)

- Semiconductors in Silicon Valley in the late 1960s and 1970s (Intel, AMD)

One way to frame YC is that by accelerating talent density, it was one of the catalyzers of the Internet golden era of Silicon Valley in the 2000s and 2010s.

Thanks to Bradford Cross for feedback on this essay